A Case Study: Chloe and Marc

Chloe and Marc are both retired and 71 years old. They are organized and intentional with their finances and looking to make the most of what they have in retirement. Let’s review Marc and Chloe’s financial standing.

- Income: Marc received a combined monthly income of $5,500 ($3,500 Social Security + $2,000 pension), while Chloe received $3,300 ($1,800 Social Security + $1,500 pension).

- Assets: Their retirement nest egg consisted of a Traditional IRA valued at $950,000 and additional savings and brokerage investments totaling $100,000.

- Expenses: Chloe and Marc had monthly expenses of $8,900, which included savings for annual expenses like property taxes and vacations.

Chloe and Marc don’t have enough monthly income (after taxes) to cover their expenses, so they have to withdraw from Marc’s IRA every month to be comfortable.

Chloe and Marc tithe 10% of their income to their local church which currently works out to be $900 per month. For years, they have given directly from their checking account and attempted to itemize their charitable contributions on their tax return. However, in recent years, it’s become harder to itemize with a high standard deduction of $30,750 (2024). Without itemizing, the charitable contributions are not deductible. However, during a financial planning review, they discovered a strategy that could significantly improve their financial situation: Qualified Charitable Distributions (QCDs).

QCDs allow individuals over the age of 70.5 to donate funds directly from their traditional IRAs to eligible charities without recognizing the distribution as taxable income. This is a significant advantage, as withdrawals from traditional IRAs are typically subject to income tax.

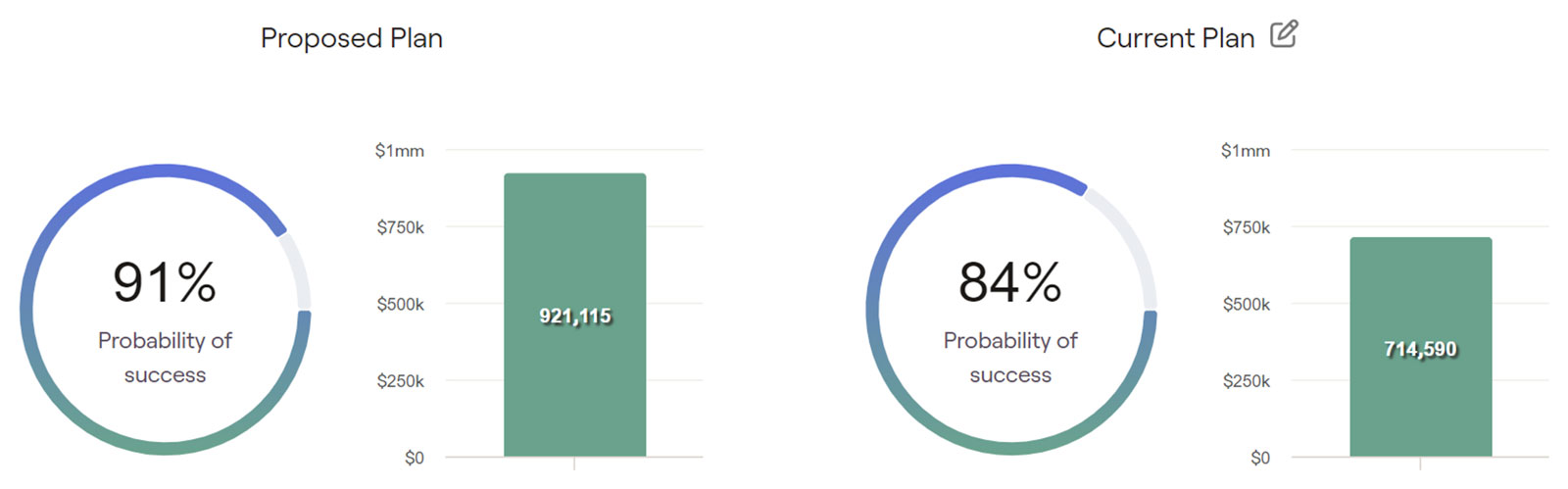

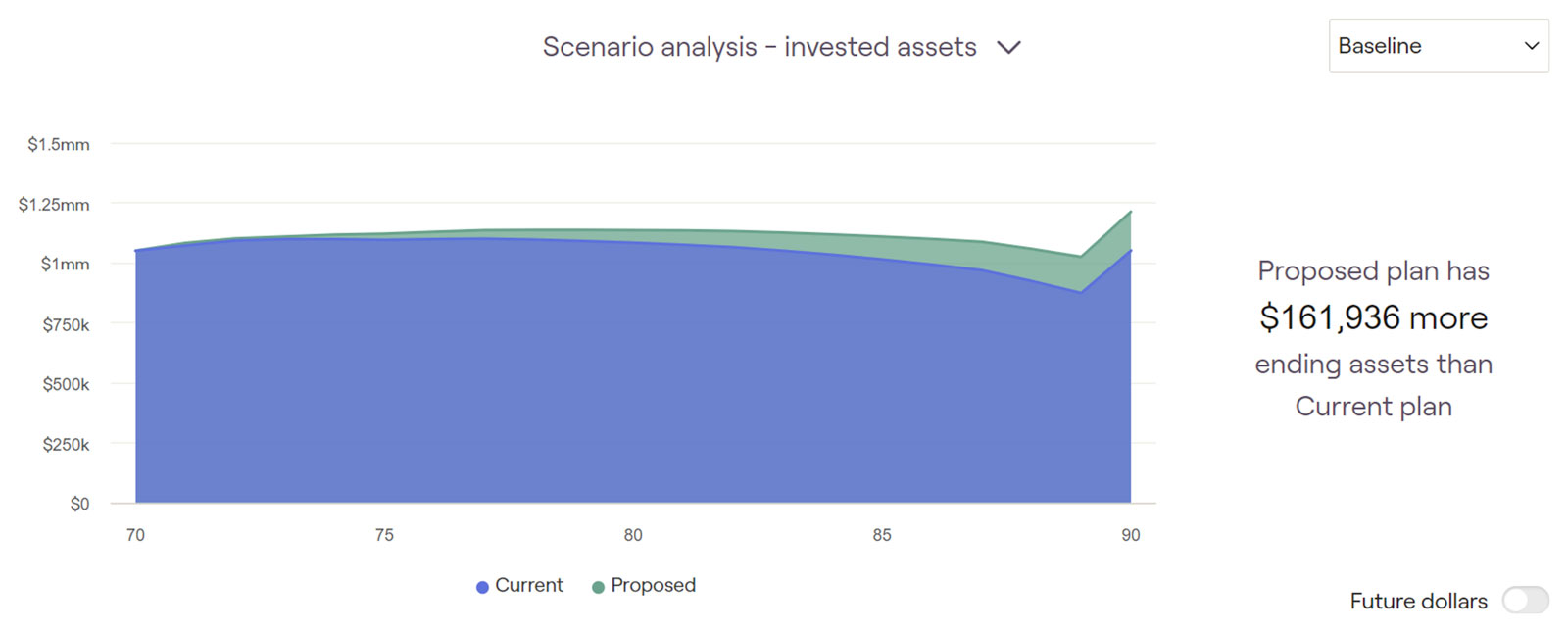

For Chloe and Marc, this meant they could reduce their taxable income while still supporting their charitable causes. By donating $900 per month directly from their IRA to their church, they could avoid paying taxes on those distributions. Now, the QCD can continue their charitable giving tax-free and their Social Security and pension income takes care of the monthly needs. This adjustment in their retirement plan improves their tax efficiency thus improving their outcome. They simply have to withdraw less to accomplish their goals, leaving more $ invested for growth over time. While Chloe and Marc weren’t at a high risk of failure in retirement, this optimization reduces the impact of potential stress tests and maximizes their generational wealth transfer.

This was especially beneficial as Marc approached the age of 73 when he would be required to start taking Required Minimum Distributions (RMDs) from his IRA. RMDs are mandatory withdrawals that must be taken from traditional IRAs starting at age 73. These withdrawals are subject to income tax, which can significantly reduce the amount of retirement income available. By using QCDs, Chloe and Marc can satisfy the Required distributions and, in turn, reduce their taxable income.

For someone who already gives regularly, QCDs can help improve the overall efficiency of a retirement plan. By reducing taxable income, Chloe and Marc could potentially withdraw less from their investments over time to meet their financial goals. This could lead to a longer-lasting retirement nest egg.

This case study demonstrates the importance of working with a financial planner to explore all available retirement income strategies. By understanding and utilizing tools like QCDs, individuals can optimize their retirement plans and ensure a more comfortable and financially secure retirement.